Is Late May the Best Time To List Your House?

You may have heard April 12-18 was the “best week” to list your house. That’s based on a report from Realtor.com. But now that it’s passed, you may be wondering if you missed your moment.

Here’s the good news – you didn’t.

Because the reality is, there isn’t just one perfect week to sell your house this Spring. There’s a window. And right now, you’re still in it.

Your Window To Sell Is Still Wide Open

Here’s why. Different organizations run studies like this every year. And they don’t always land on the exact same week. That’s okay. It’s because they’re using different research methods and even different definitions of what “best” means.

But the fact that the results vary points to a larger trend. While there may be sweet spots, the entire Spring season gives sellers an opportunity to get some of the best conditions (and best sales prices) of the year.

And it’s definitely not too late to jump in.

Why Listing in Late May Is the Perfect Play

According to Zillow, the best time to list your house this year is the last 2 weeks of May. And that’s approaching fast.

Based on their analysis, this is the ideal time to do it if you want to make top dollar. Because, in this 2-week window, homes sell for more. Sometimes, quite a bit more.

Depending on where you are and the price point in your area, some homeowners may even net tens of thousands of dollars extra in this sweet spot. As Zillow explains:

“Why late spring? Buyer demand typically peaks before Memorial Day. Families want to move during the summer and settle in before the new school year. More buyers shopping at once can spark competition and lift prices.”

And they’re not the only ones saying listing in May could be the key to selling for more. ATTOM Data analyzed almost 52 million home sales over the past 10 years and found sellers in May are achieving some of the highest returns.

That means the ideal window this year is very much still open.

What This Means for You

If your goal is to sell for the strongest possible price, this is where timing and strategy come together. And you want to be sure you’re ready to make the most of it.

So, what should you be doing right now?

When prepping for a fast-moving window like this, you don’t want to waste time or money on the wrong prep work. And your agent is your go-to to make sure you’re focusing on the right things.

They’ll be able to tell you if the “best week” is slightly different in your market. And what quick repairs or updates can help you get a higher price, without taking a ton of time or effort.

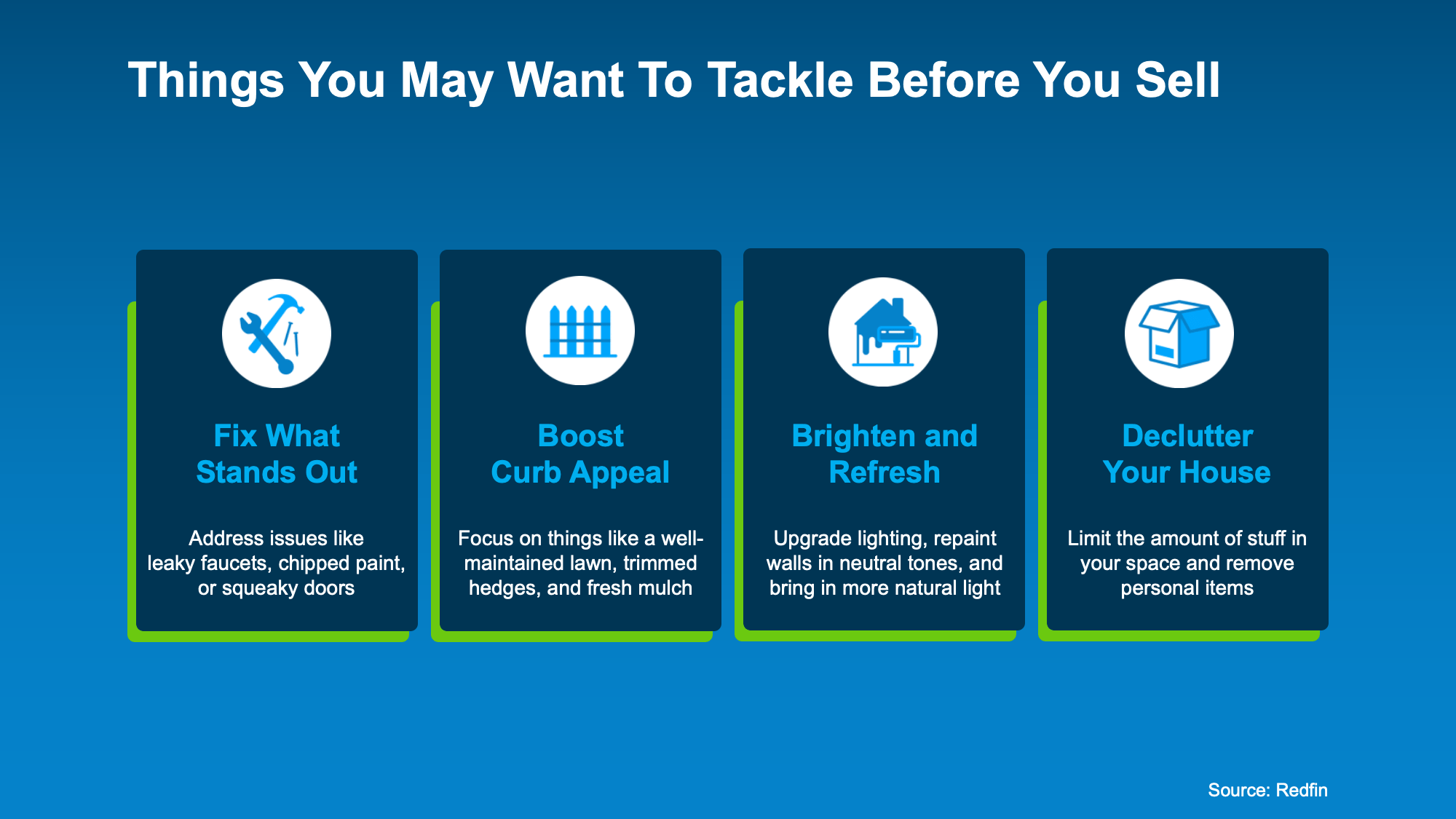

Here’s a quick example of things an agent may recommend based on information from Redfin:

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

Bottom Line

Zillow says the best time to list your house is just around the corner. Are you ready to make the most of it?

If you want to take advantage of this Spring sweet spot and get top dollar for your house, talk to a local agent about what you need to do now to get ready to hit the market.

#fidelityhomegroup, #floridamortgage, #floridamortgagerates, #mortgageflorida

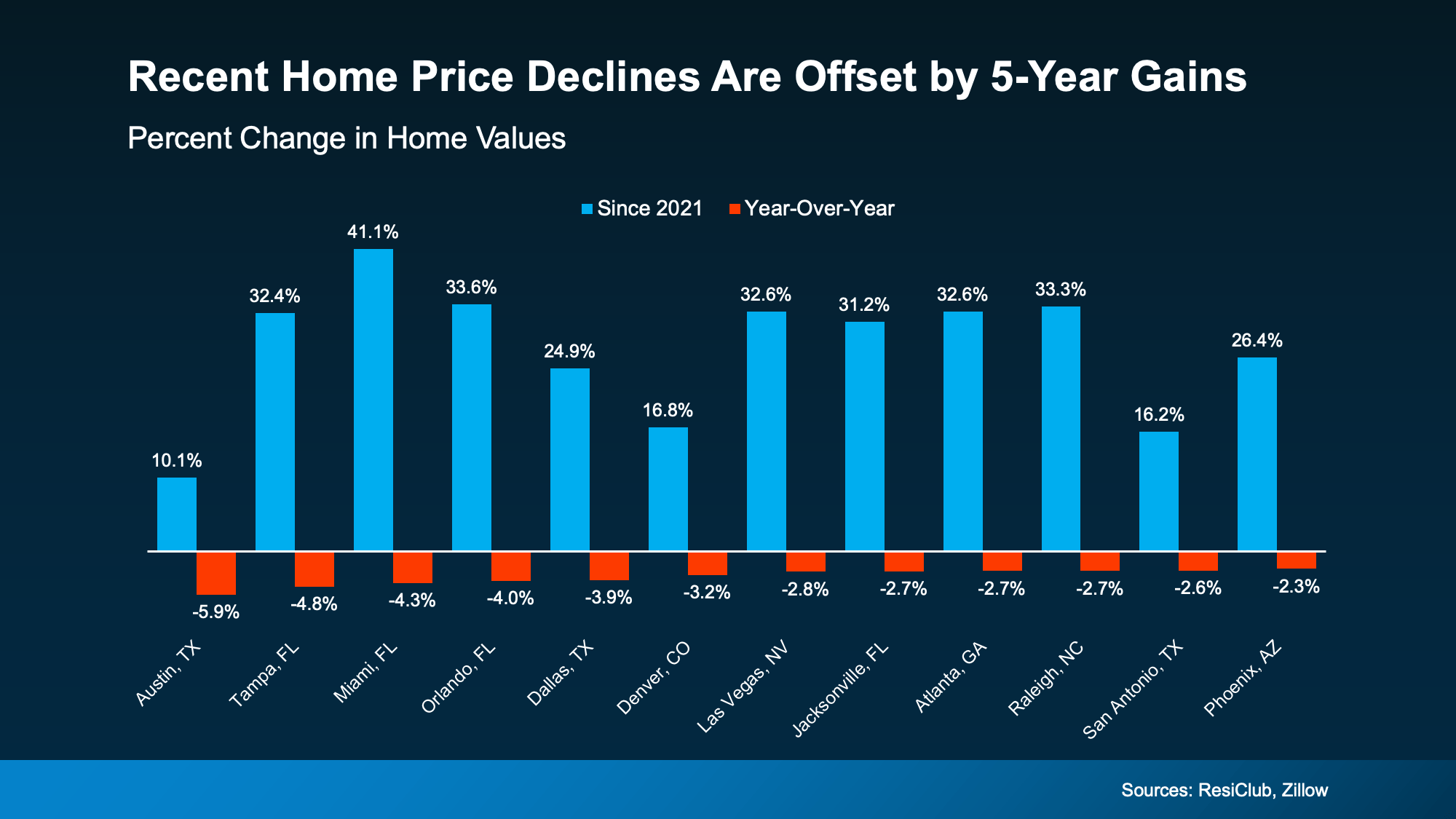

While it can vary a lot based on where you live, only

While it can vary a lot based on where you live, only  That’s not a crash. That’s just prices moderating after a few record-breaking years.

That’s not a crash. That’s just prices moderating after a few record-breaking years.