Lower Asking Prices Are a Win for Today’s Buyers

If affordability has been the biggest thing standing between you and a home, there’s a little good news.

Asking prices have started to come down.

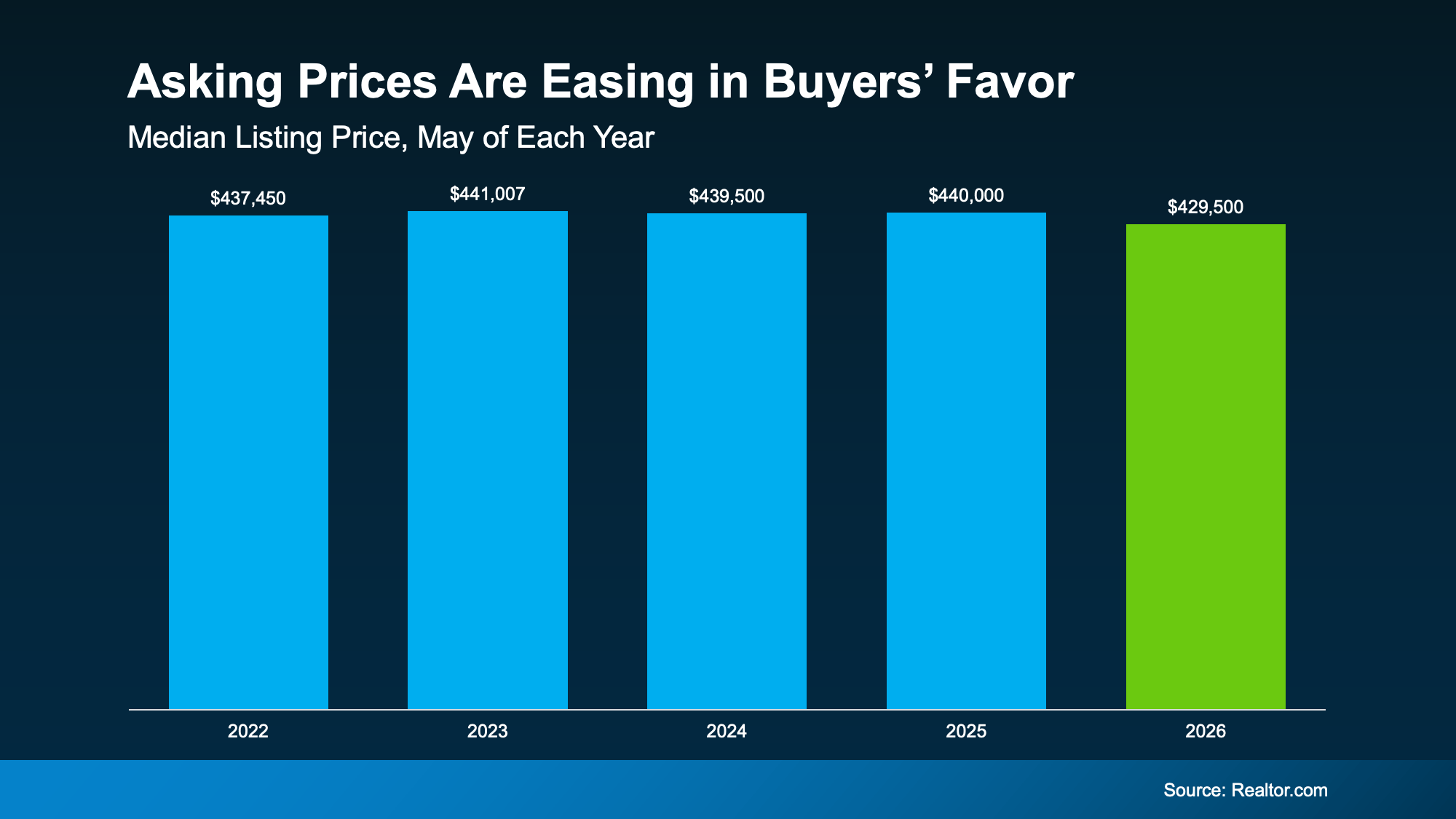

The typical seller listed their house for a median of $429,500 in May. That’s 2.4% lower than a year ago, according to Realtor.com. On its own, that won’t transform what you can afford, but in today’s market every little bit helps and it signals a broader shift taking place.

Buyers Are Finally Catching a Break

Check out this data from Realtor.com and you can see this is the first May in years where buyers have caught any sort of break price-wise.

Each May from 2022-2025, things held pretty steady. But this year? You can see that more noticeable shift in your favor (see graph below):

While the dip from $440,000 to $429,500 isn’t a big one, it gives you more breathing room. And that’s not a small thing when affordability has been this tough.

Now, lower asking prices don’t mean every home is suddenly within your range. But they do show buyers are gaining a little ground.

And in today’s market, a little ground can go a long way.

What That Means for the Housing Market

And just in case this crossed your mind, this is good news for your move, not bad news for the market as a whole.

The subtle dip from last May to this one shows prices are easing, but they’re not dropping off a cliff. What this is actually a sign of is that the market’s rebalancing now that the number of homes for sale has grown.

Buyers have a bit more power again, and sellers know they can’t name just any price and expect their house to sell. They either meet the market where it is, or face a price cut later. And in general, sellers would rather avoid a price cut. As the New York Post explains:

“Rather than swinging for the fences with pandemic-era price tags, sellers are increasingly coming to terms with a new reality. The share of listings featuring price cuts actually fell to 17.5% in May, suggesting homeowners are doing their homework before putting up a “For Sale” sign instead of chasing unrealistic numbers and cutting later.“

This signals a broader change in the market.

Seller expectations have been skewed a little high since the pandemic buying frenzy – you’ve probably felt that firsthand. But now, things are starting to normalize. It could mean less back-and-forth to land on a fair number. And homes should be priced a bit more realistically from the start.

Bottom Line

If affordability has been your top concern, the recent dip in prices is an opening. Connect with a local real estate agent to see what that looks like in your area.

#fidelityhomegroup, #floridamortgage, #floridamortgagerates, #mortgageflorida

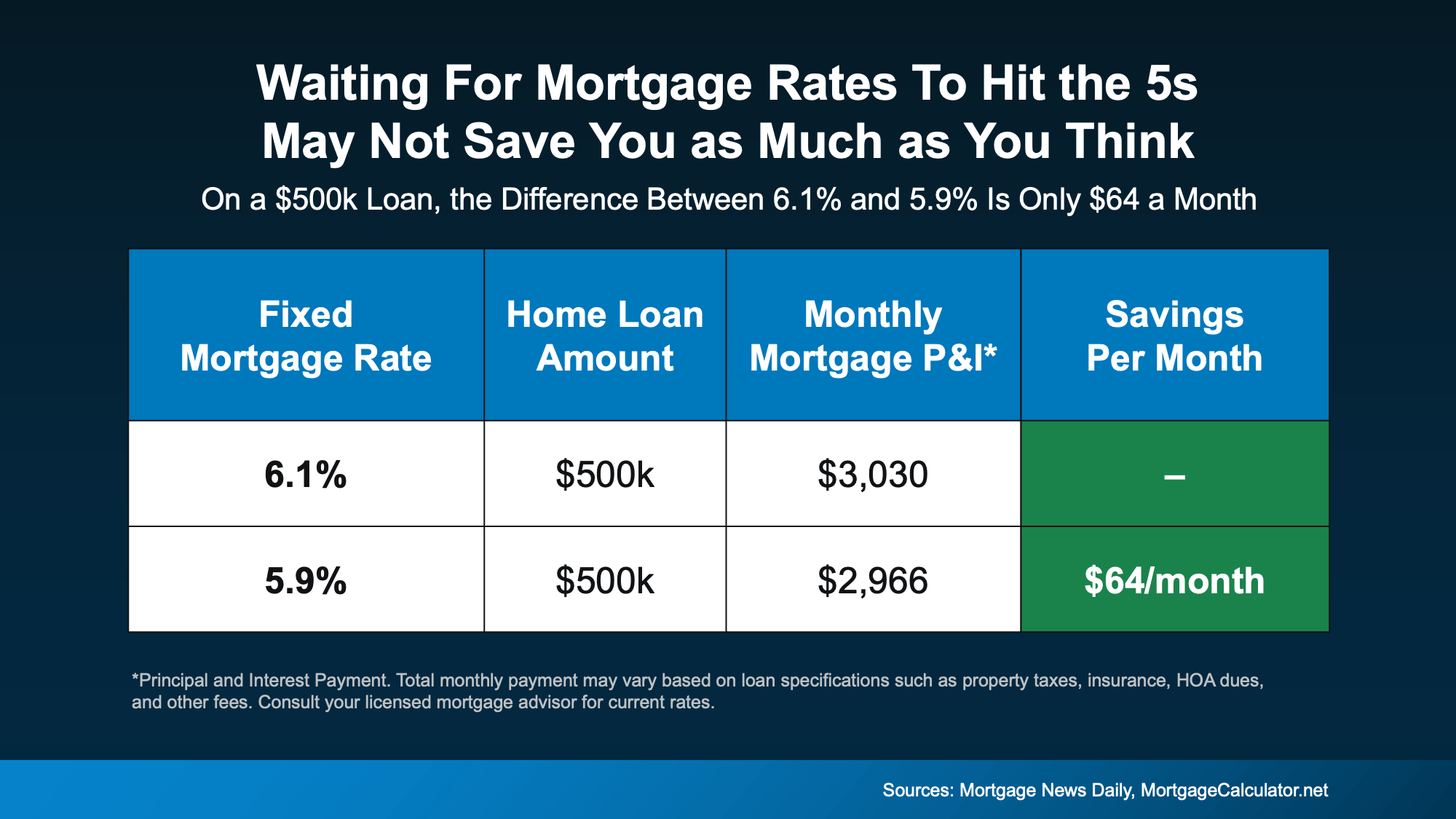

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.

Sure, your monthly payment would’ve been a little less expensive a few weeks back. But hindsight is always 20/20.