Two Big Reasons To Move This Summer

A lot of people who want to move are telling themselves the same thing: “Maybe I’ll just wait until later this year once things calm down.”

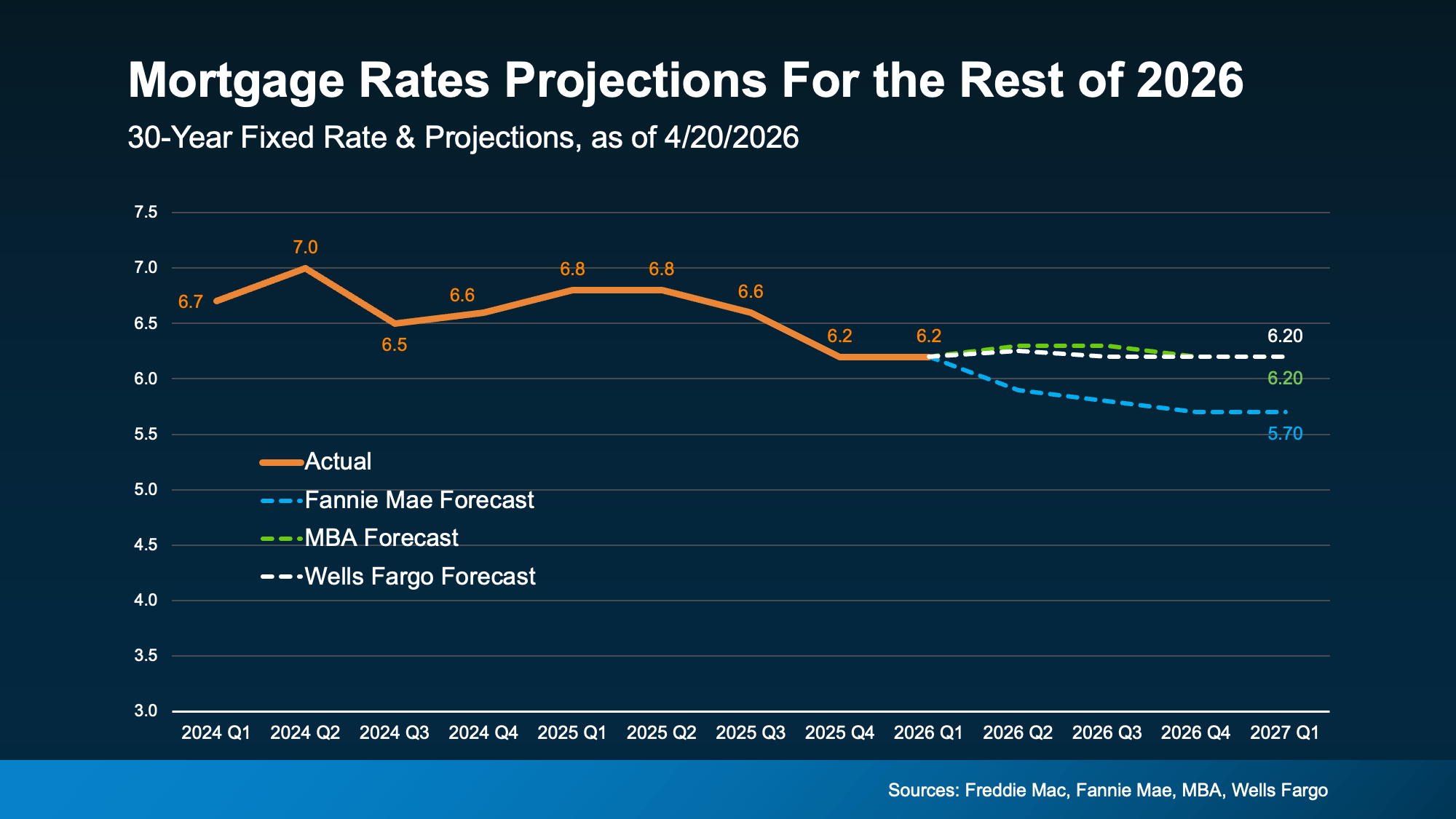

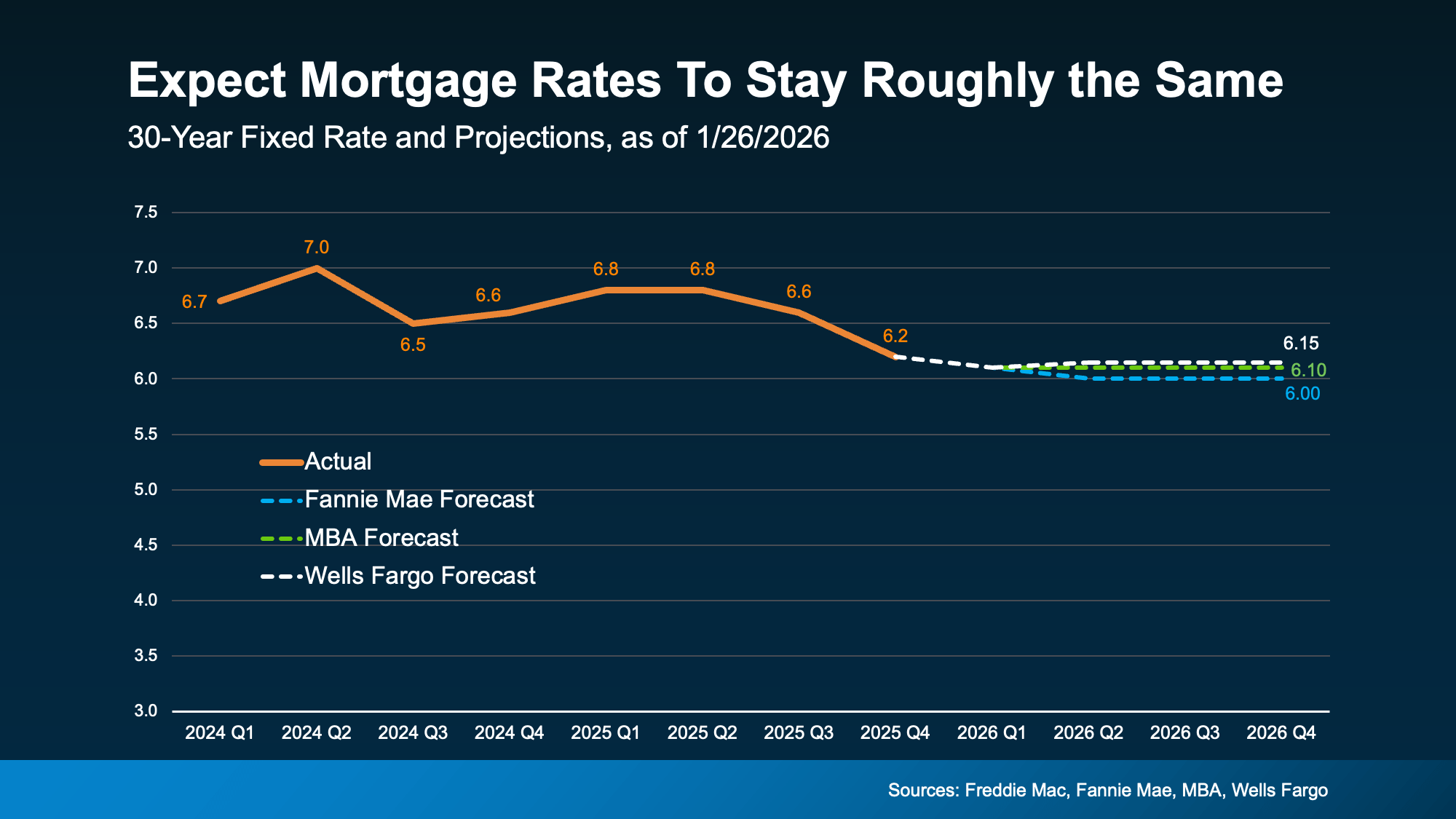

While waiting sounds like a good plan, there’s something worth knowing before you decide. Rates aren’t expected to change much, so if that’s the #1 reason you’re waiting, it may not pay off. And there may be other things you miss out on in the meantime.

Historically, Summer is one of the strongest seasons of the year for both buyers and sellers. And if you delay your move until Fall or Winter, some of those opportunities may already be fading.

Buyers: Fresh Inventory Is Your Real Summer Advantage

One of the biggest frustrations buyers have faced over the past few years has been a lack of affordable options. Maybe you’ve run into that yourself:

You find a house you like, but it’s out of your budget.

You find something in your budget, but you don’t like it.

Or worse, nothing interesting hits the market for weeks.

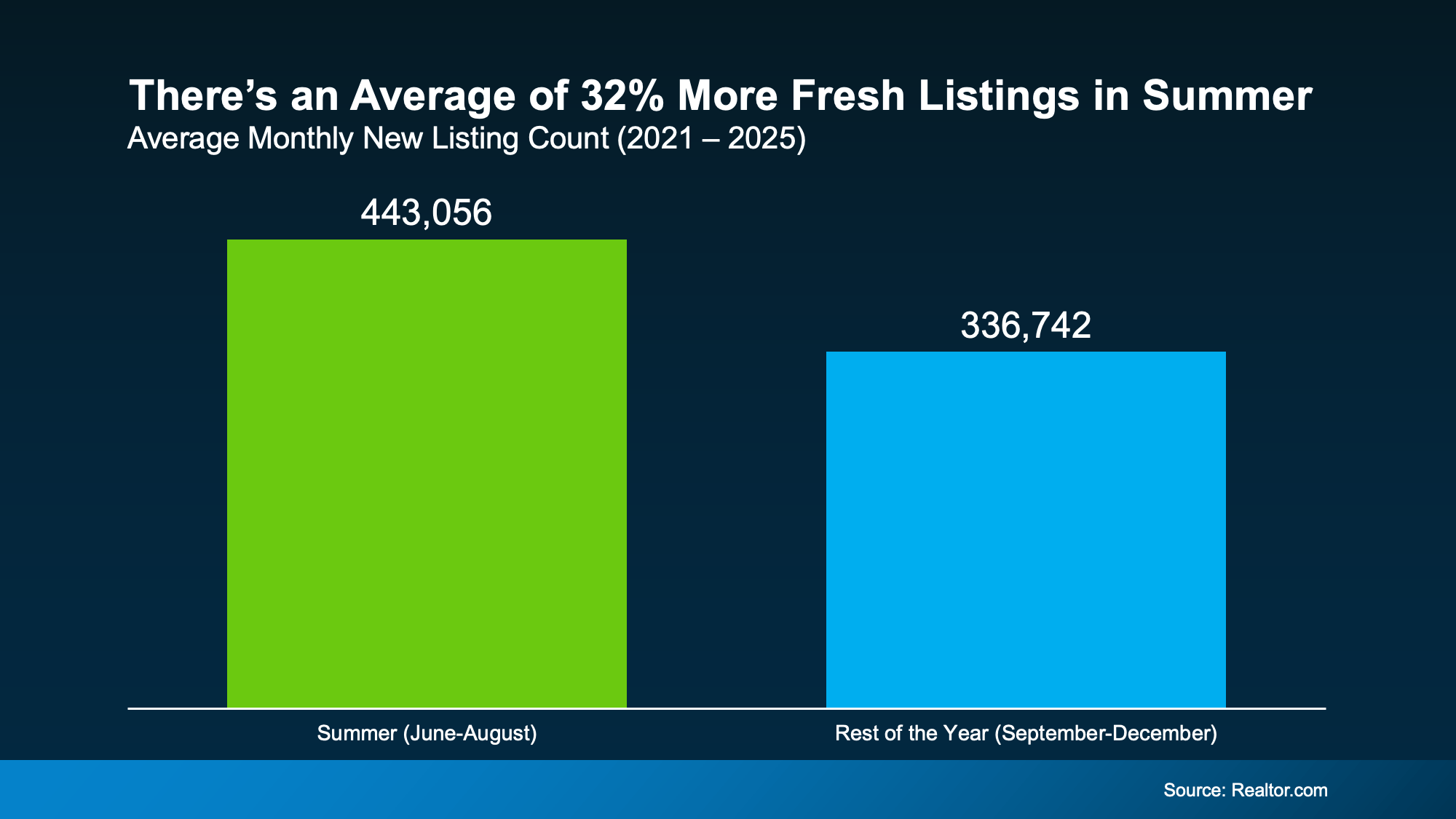

Historically, Summer helps with that.

Looking at data from the last few years, Summer months consistently bring more sellers into the market than later in the year. And that gives buyers a real window of fresh choices.

According to Realtor.com, any given Summer month typically sees about 32% more fresh options than the average month from September-December.

With more newly listed homes, there’s a better chance of finding one you like where the numbers actually work.

Because all it really takes is one home to completely change your search. And if you’ve got more popping onto the market to choose from, maybe one of those is exactly what you need.

But keep in mind, this seasonal window isn’t open forever. Fresh inventory tends to slow down once Summer ends.

Many homeowners who planned to sell this year have already listed by then. Families who wanted to move before school starts have often already gotten it done, or at least, set it into motion. So, new listing activity usually cools as we head into Fall and Winter.

Of course, every year is different. But if finding the right home at the right price has been your biggest challenge, waiting until later in the year may not necessarily give you more options. In fact, recent history suggests it may do just the opposite.

Sellers: Homes Usually Sell for More in the Summer

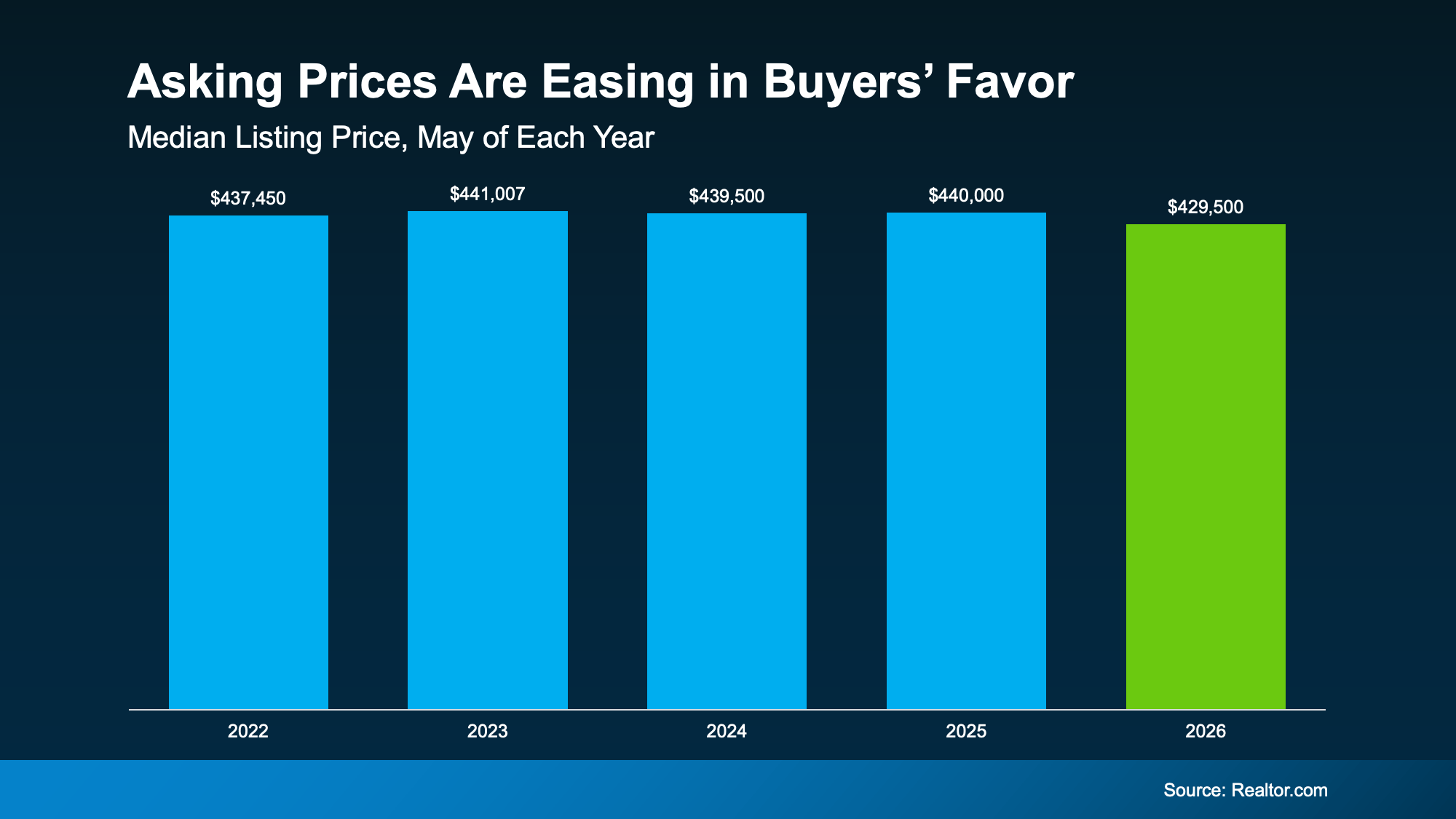

If you’re thinking of selling, you may be considering holding off because you’ve seen headlines about lower asking prices, price cuts, and softer conditions in some markets. But those headlines don’t tell the whole story or convey just how much it varies by area.

Here’s what you really need to know. Even though the market’s becoming more balanced and some pockets are experiencing price declines, that doesn’t mean you’ve missed your chance to sell.

Seasonality can still work in your favor no matter where you are. And this Summer could still give you the chance to sell for a good price.

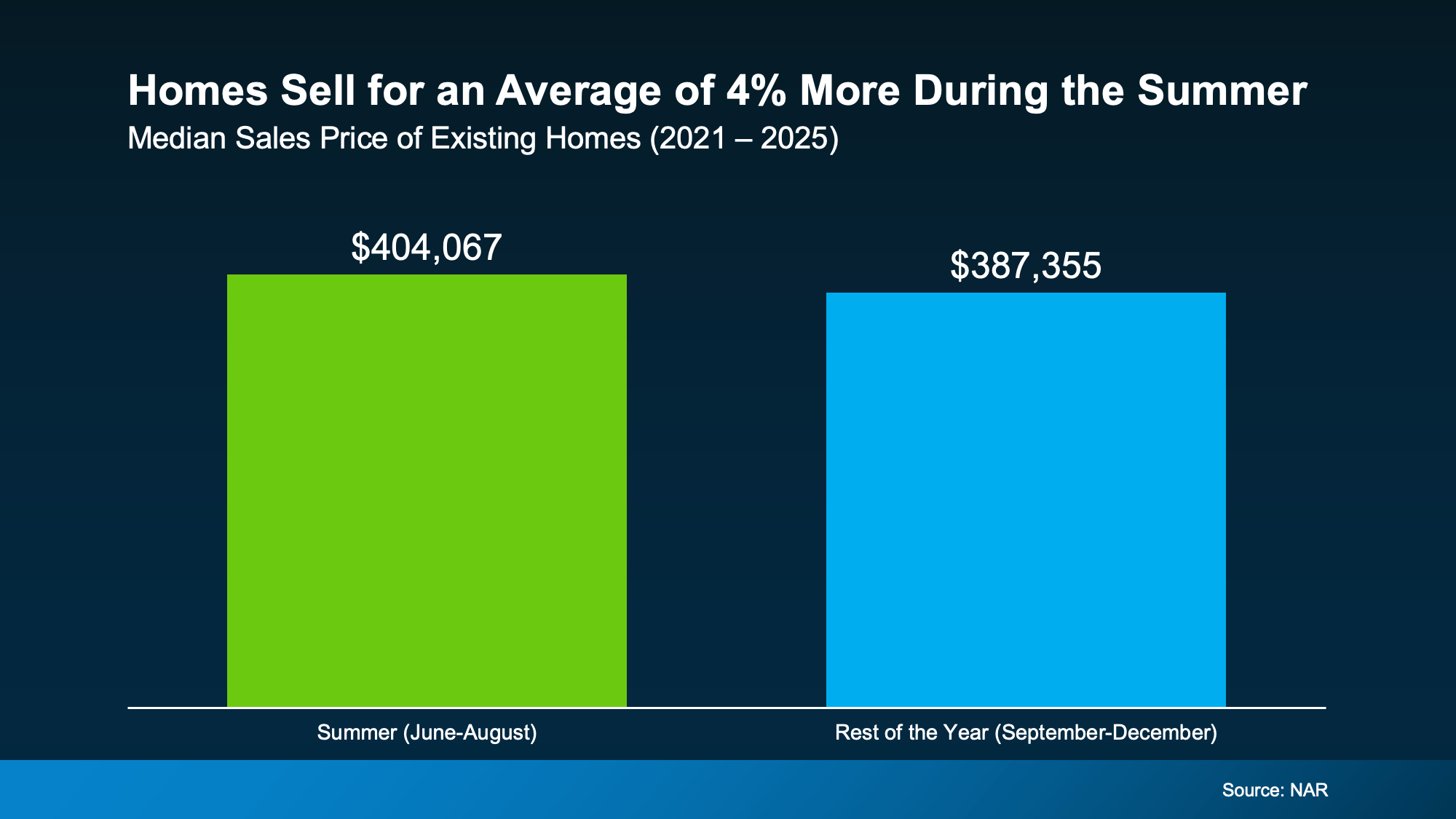

According to the National Association of Realtors (NAR), homes sold during a Summer month usually sell for about 4% more than homes sold during the typical month from September-December:

Why? Summer buyers are usually operating on a set timeframe. They’re trying to move before the next school year or when they have more PTO and warmer weather to tour houses. That urgency can translate into better offers.

Now, that doesn’t mean you should price your house 4% higher this Summer. That would actually be a mistake in today’s market.

It just means if you’re looking to get as much for your house as you reasonably can, a Summer move could be a smarter play than waiting until later this year.

Because based on typical seasonality, you may get more for your house than you would if you waited until the Fall or Winter (when there are typically fewer buyers active).

And if you’re considering a move anyway, that’s worth factoring in.

Bottom Line

Could waiting until later this year work out? Sure. But it’s important to understand what you may gain by moving now too – that way you have the full picture before you decide.

If a 2026 move is on your radar, talk to an agent about what matters most to you. Depending on your priorities, Summer could be your moment.

#fidelityhomegroup, #floridamortgage, #floridamortgagerates, #mortgageflorida

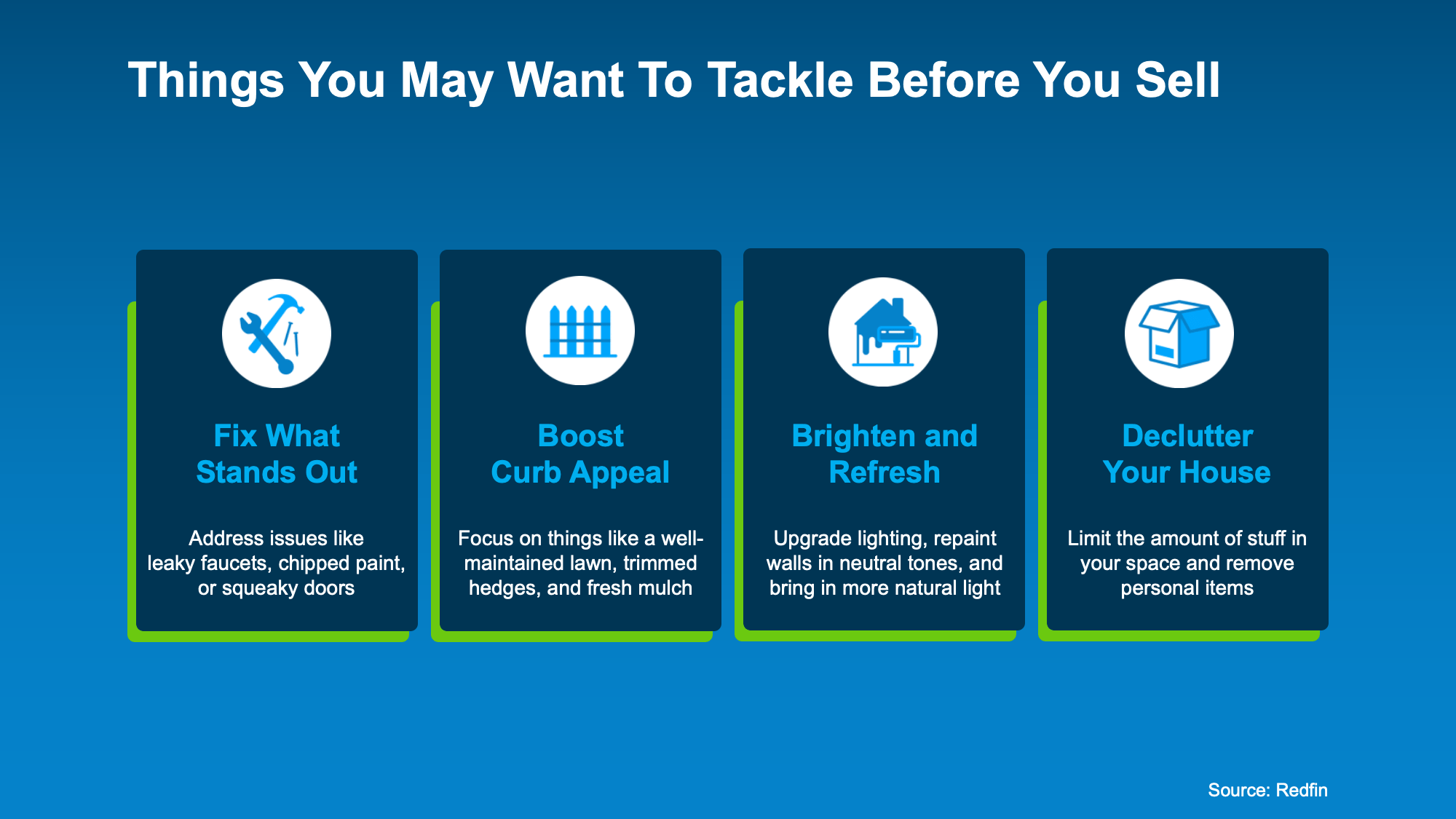

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

At the end of the day, when your prep time’s short, doing the right things matters more than doing more things.

While it can vary a lot based on where you live, only

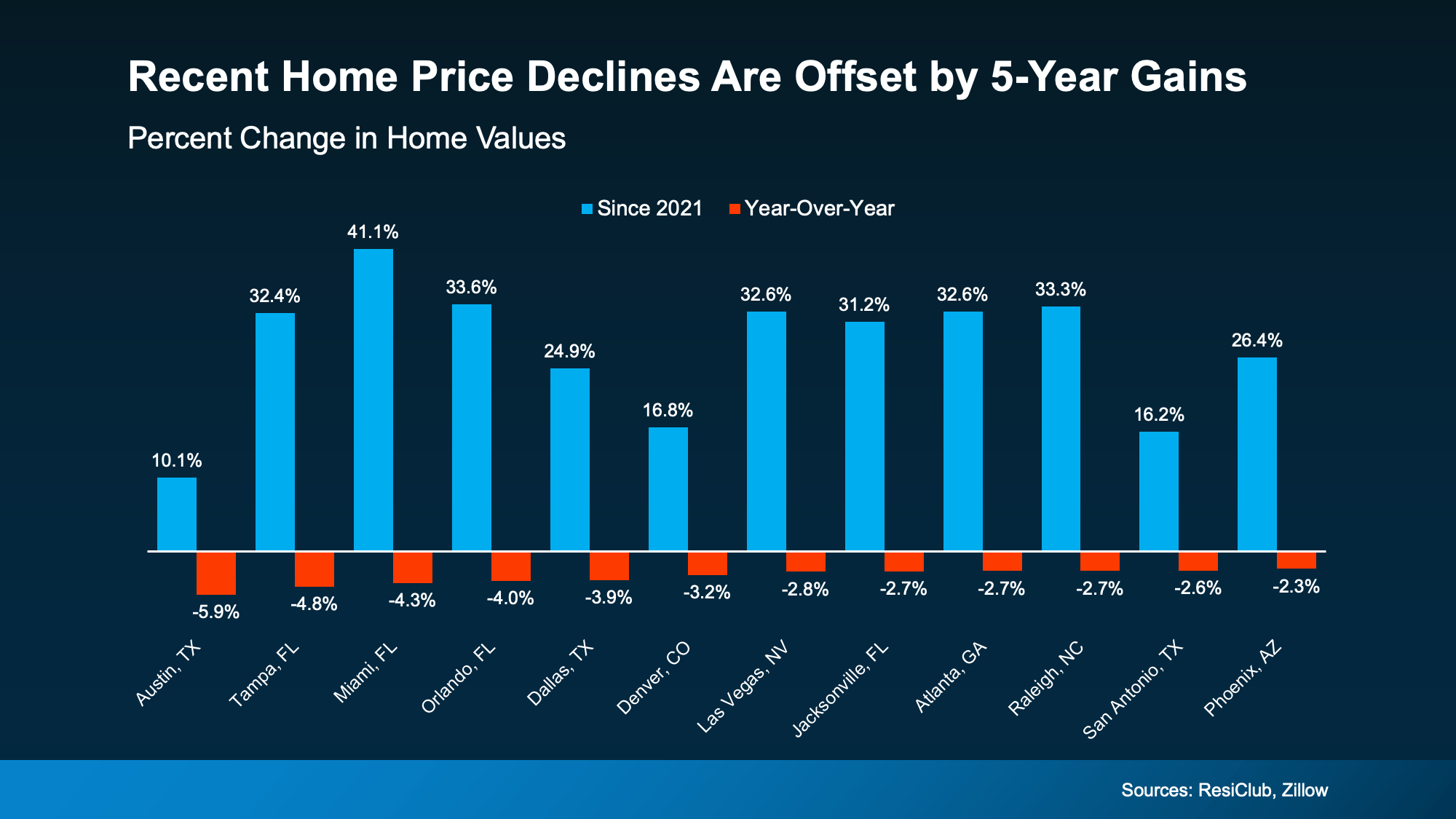

While it can vary a lot based on where you live, only  That’s not a crash. That’s just prices moderating after a few record-breaking years.

That’s not a crash. That’s just prices moderating after a few record-breaking years.

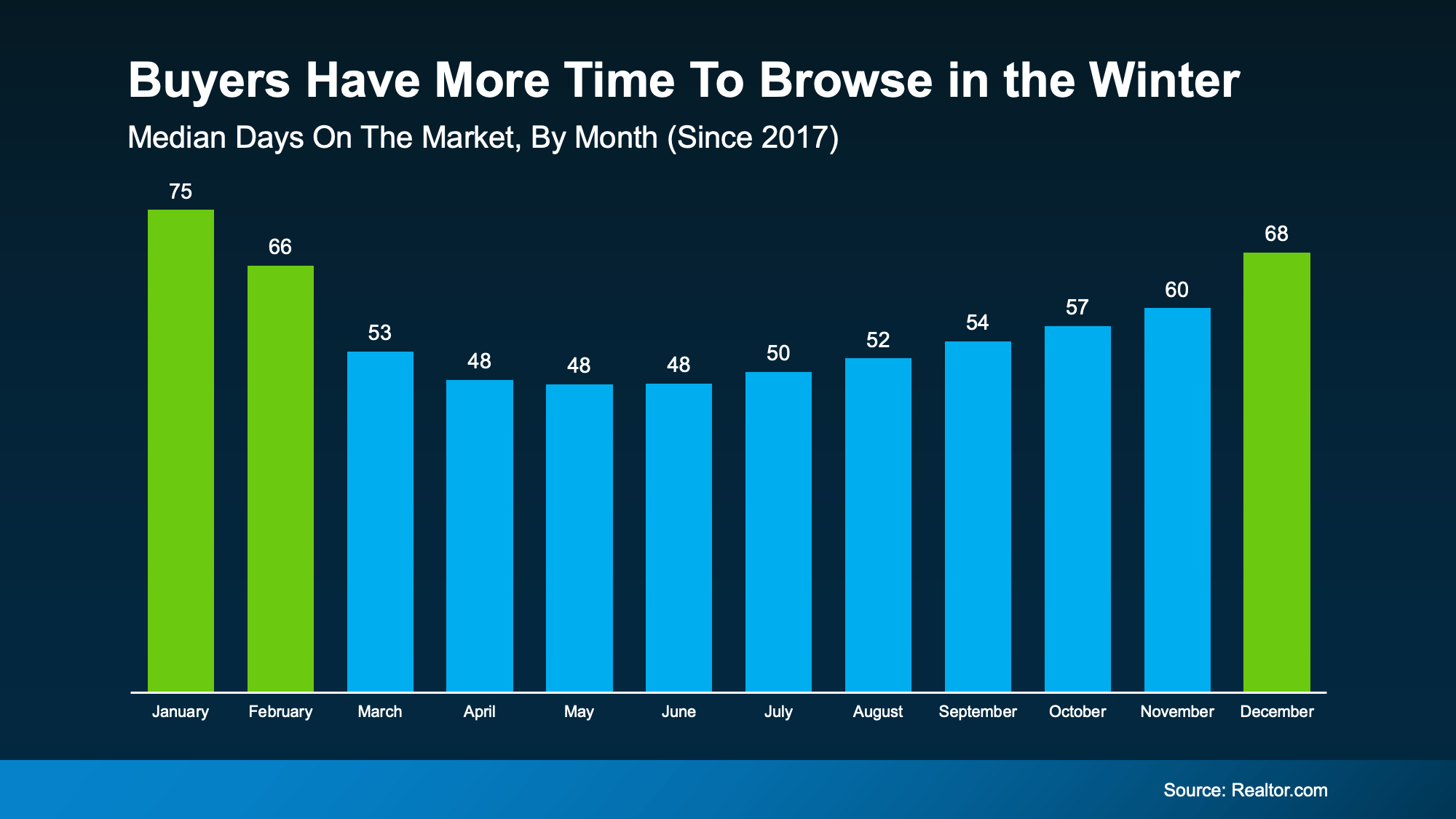

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.