A few years ago, sellers could get away with saying “no” to just about everything.

No repairs.

No concessions.

No negotiation.

If buyers wanted the house, they pretty much had to take it on the seller’s terms. But now that inventory’s grown, negotiations are becoming a normal part of the process again.

That’s why one of the most important things sellers need to understand right now is this:

The goal isn’t to “win” every negotiation.

Sometimes, it’s worth meeting buyers where they are to get a deal done, fast. One example? Helping with a buyer’s closing costs.

Let’s break that down, so you know what to expect if it comes up in your sale.

What Are Buyer Closing Costs?

Closing costs are the extra expenses buyers pay on top of their down payment when they purchase a home. Freddie Mac gives some examples:

Typically, buyer closing costs range from about 2% to 5% of the home’s purchase price. So, on the typical $400,000 home, that could mean anywhere from $8,000 to $20,000 out of pocket.

And in today’s affordability-challenged market, that upfront cash can be a major hurdle for some buyers – even if they can comfortably afford the monthly mortgage payment itself.

That’s why more people are asking sellers for help.

And More Sellers Are Saying “Yes”

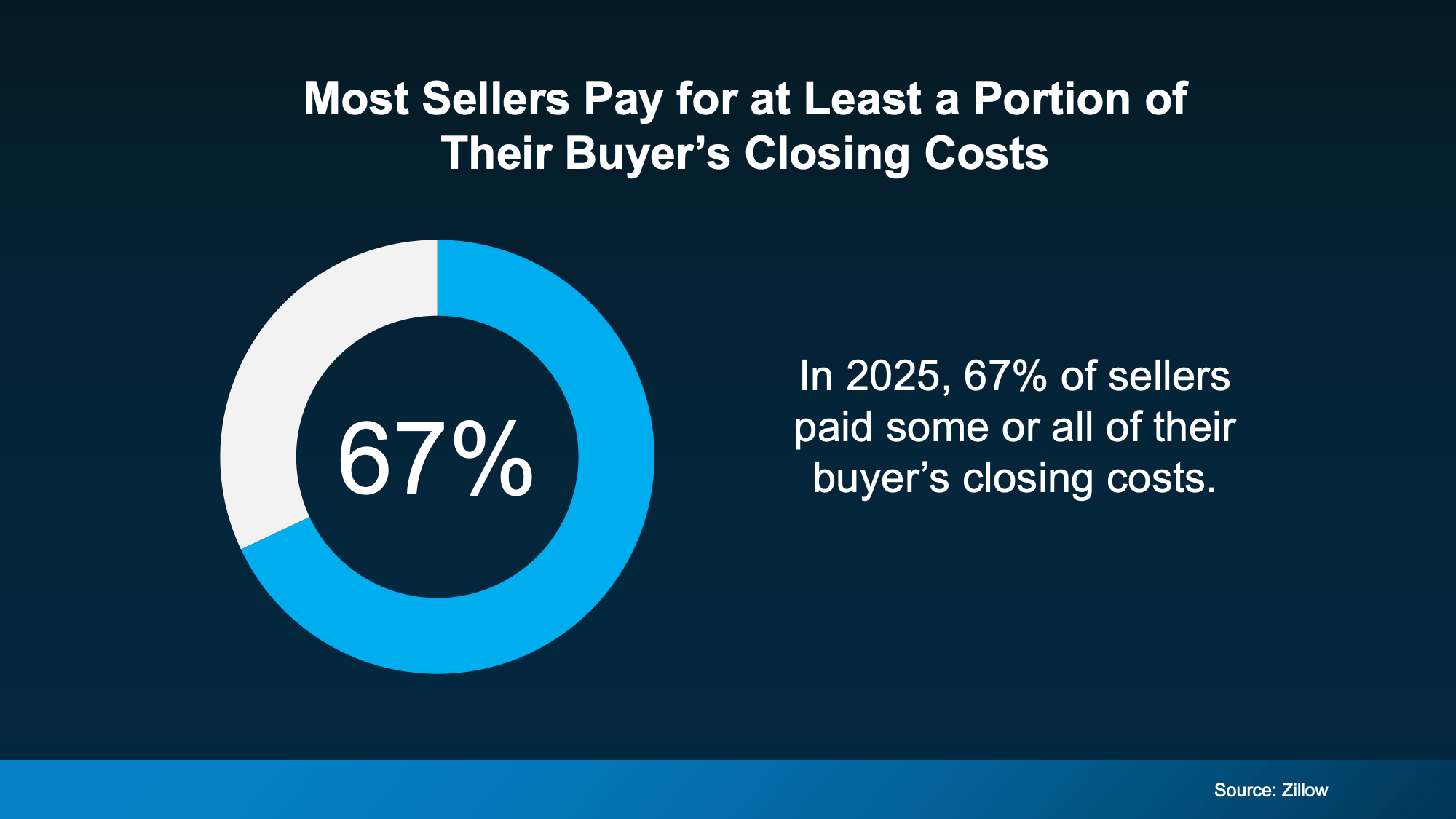

According to the latest data from Zillow, 67% of sellers reported paying some or all of the buyer’s closing costs in 2025 (see chart below):

Now, that doesn’t mean every seller is doing it. And it definitely doesn’t mean every seller should. But it does show how common concessions have become as the market has shifted. And that’s important for you to know.

When Paying Closing Costs May Make Sense

This is where many sellers get stuck. They hear “help with closing costs” and immediately think: “Why should I pay for their expenses?”

But that’s not always the right way to look at it. You’ve got to consider who has the leverage in today’s market.

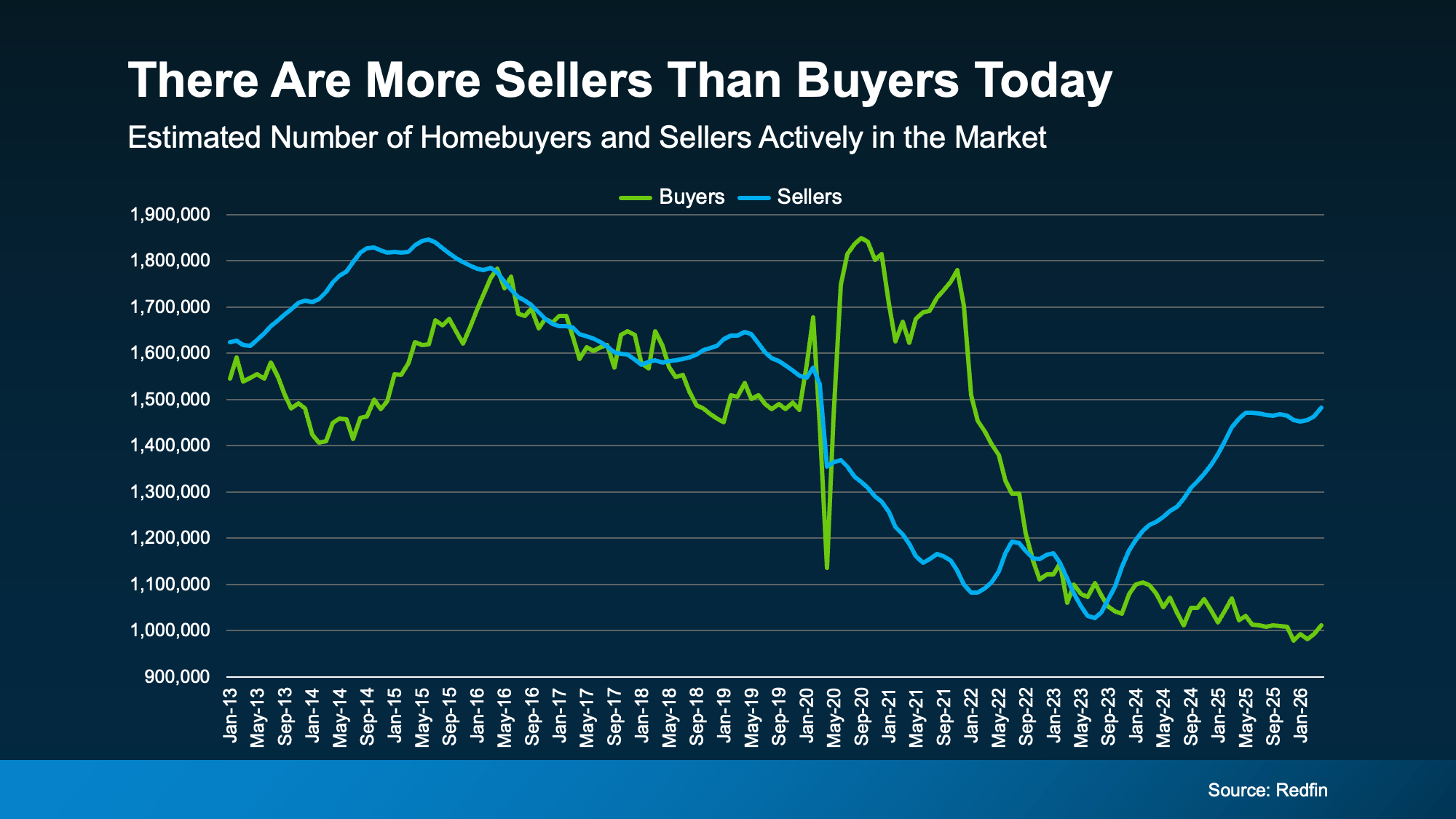

Redfin data shows there are more sellers than buyers active today. And that shifts the market dynamics (see graph below):

That doesn’t mean every market favors buyers. Far from it. In some areas, homes are still selling quickly and sellers have plenty of leverage. But in others, buyers have more room to negotiate than they’ve had in years.

That’s why local market conditions matter so much when you make your decision.

For example, helping with closing costs may be worth considering if:

There are a lot of homes for sale in your area

Your house has been sitting on the market longer than expected

You’ve had showings, but no offers

You’re motivated to move quickly

Or you’re trying to keep a deal together during negotiations

After all, if it’s the thing that helps bring a serious buyer across the finish line, it could be well worth it.

Other Concessions You Could Offer Instead

Just remember, being flexible doesn’t mean saying “yes” to every request. It means understanding which compromises actually help you accomplish your goals. Because there are always alternatives.

Redfin suggests considering other concessions if you’re not interested in helping with closing costs, like:

The right answer depends on what buyers in your market are asking for and what matters most to you. That’s exactly why working with an experienced local agent is so important.

Bottom Line

The sellers having the most success today are the ones who understand the market has changed and are adapting to meet it where it is.

Sometimes that means negotiating on closing costs. Sometimes it means offering something else. The key is knowing which concessions are worth it for your local market.

If you’re wondering what’s normal in your area, what’s worth negotiating, and where it makes sense to stand firm, connect with an agent.