Eco-Friendly, Energy-Efficient Homes Attract Buyers

Are you planning to sell your house? If so, you may be surprised to hear just how much buyers value energy efficiency and eco-friendly features today. This is especially true as summer officially kicks off.

In fact, the 2023 Realtors and Sustainability Report from the National Association of Realtors (NAR) shows 48% of agents or brokers have noticed consumers are interested in sustainability.

So, if you’re considering selling your house, why does this matter to you? It helps you know what you can do to make your house even more appealing to today’s buyers. According to Jessica Lautz, Deputy Chief Economist and VP of Research at NAR:

“Buyers often seek homes that either lessen their environmental footprint or reduce their monthly energy costs. There is value in promoting green features and energy information to future home buyers.”

Consider Upgrading Your Home To Make It More Appealing

If you want to upgrade your house in a way that maximizes its green appeal, you need to work with a local agent to understand what buyers in your area are looking for. The same NAR report identifies the following green home features as most important to buyers at a national level:

- Windows, doors, and siding

- Proximity to frequently visited places

- A comfortable living space

- A home’s utility bills and operating costs

While you can’t change the location of your house, you can take action to make sure it’s as comfortable as possible while also setting up the next owners for lower operating costs. ENERGY STAR shares some suggested upgrades as ones that may be worth considering:

- Heating and cooling: Ensure your HVAC system is properly maintained and regularly serviced to maximize its efficiency. Consider upgrading to a high-efficiency model, if needed.

- Water heater: Your water heater uses a lot of energy. Upgrading to a heat pump water heater can significantly reduce energy consumption and appeal to environmentally conscious buyers.

- Smart thermostat: A big part of your energy bill goes to heating and cooling. Install a programmable thermostat to better regulate temperature settings. This not only enhances comfort but can also lower energy usage.

- Attic insulation: Proper sealing and insulation in your attic help prevent air leaks and maintain a comfortable temperature, reducing the strain on heating and cooling systems.

- Energy-efficient windows: Replacing old, drafty windows with energy-efficient ones can minimize heat transfer and lower your energy bills.

It’s worth noting that you may be able to take advantage of tax credits and rebates for energy-efficient home installations and upgrades. These incentives could help offset a portion of the costs associated with eco-friendly home improvements.

As you prepare to sell your house, it’s important to recognize that real estate agents are valuable resources. They can help you determine which upgrades would be most appealing for buyers in your area and provide guidance on which green features to highlight in your listing. If you’ve already made these updates recently, tell your agent so they can feature them in your listing.

Bottom Line

Focusing on energy efficiency and eco-friendly features can help make your house more appealing to buyers today. Connect with a local real estate agent to ensure you’re choosing the right upgrades for your area.

#fidelityhomegroup, #floridamortgage, #floridamortgagerates, #mortgageflorida

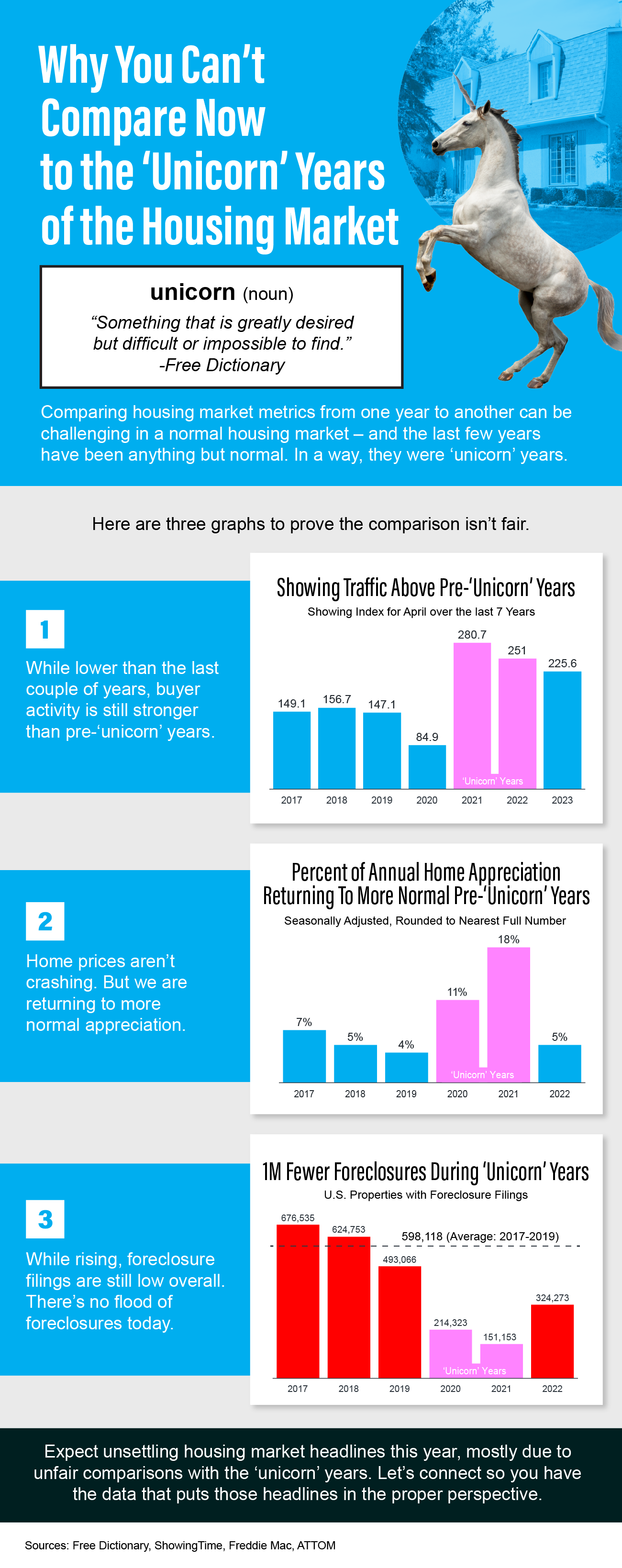

![Why You Can’t Compare Now to the ‘Unicorn’ Years of the Housing Market [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230608/Why-You-Cant-Compare-Now-to-the-Unicorn-Years-of-the-Housing-Market-KCM-Share.png)

![Moving Now Can Give Your House Its Day in the Sun [INFOGRAPHIC] Simplifying The Market](https://files.keepingcurrentmatters.com/content/images/20230525/Moving-Now-Can-Give-Your-House-Its-Day-In-The-Sun-KCM-Share.png)